“The digital age is transforming corporate treasuries as data, speed and automated cost controls are prioritized. Banks and supply chain partners must also transform to help the function become a value-addition to the business that can dynamically spot risks, opportunities and threats,” says Sumit Aggarwal, Executive Vice President and Group Head – Transaction Banking Services (TBS) at Emirates NBD.

The days of just conducting cash management are over as digital transformations (DX) proliferate at banks and corporations. As Arun Singh, Corporate Treasurer at Aramex, a global logistics firm listed on the Dubai Financial Market (DFM) with revenues of over AED 5,086 mn in 2018, says: “A treasurer’s role is becoming more strategic, and our remit is expanding. Increasingly we’re expected to contribute over and above the norms of previous decades. Technology is becoming the single biggest enabler in helping us meet this challenge.”

“Partners matter too”, adds Arun. “Selecting and implementing the correct technological fit from the huge array of available solutions is the key for treasurers.”

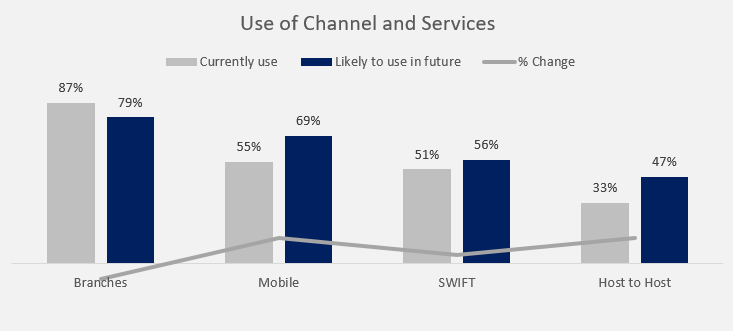

Cashless RTP-enabled domestic payments and fast global payments and collections – often using SWIFT’s cross-border global payments are on the horizon, as is the use of mobile tools and digital ways of working for all treasuries. This trend was illustrated in a recent survey of 120 corporate practitioners by Greenwich Associates on behalf of Emirates NBD. It showed that branch-based banking is diminishing in importance for corporate treasurers as digital alternatives emerge.

Figure 1: Branch-based banking is waning in popularity with treasurers as digital alternatives arise. Source: Greenwich Associates, MENA Survey for Cash Management, Emirates NBD, 2019.

Digital infrastructure upgrades are encouraging data driven invoicing and payment practices. These can feed into practical corporate liquidity, loan and working capital solutions that deliver treasury benefits.

The entry of Fintechs in the UAE is driving efficiencies in visibility, cost control and speed through new data tools. These nimble new Fintech start-ups often work in conjunction with banks, companies or established technology vendors who provide them the scale and make use of their solutions to achieve maximum efficiency.

The benefit of collaborating with innovative start-ups to incumbent banks and other financial players is that they can retain their share of wallet with corporate treasury clients while assisting them – and their internal IT departments – in their Digital Transformation journey.

Start-ups typically lack the investment dollars needed to scale up, so they benefit from the relationship as well. They can help banks and treasuries overhaul their legacy IT systems and siloed operations and simultaneously find a market for their solutions.

It’s a win-win symbiotic relationship that enables established firms to digitize quickly and move away from legacy paper-based systems, while Fintech start-ups get customers.

Dubai Fintech incubators:

The Dubai Financial Services Authority (DFSA) is inviting global Fintech firms to apply for an Innovation Testing License (ITL) to develop and test new concepts in a live, but a restricted environment, which protects customers before extensive rollouts are permitted.

In March 2019, Emirates NBD partnered with DIFC FinTech Hive to launch a new program where the bank is certifying Fintechs that collaborate, co-create and innovate using the bank’s application programming interface (API) Sandbox.

Futureproofing and innovation

The competitive element in the financial services (FS) sector of the future will be witnessed in the services layer, not the digital infrastructure layer. Enhancing the data visibility, transparency, speed and service to the end-user is vital for successful firms that want to ensure tech-savvy newcomers don’t diminish their role.

Data utilization

Fintech developed data tools can be used by treasurers to dynamically price a loan more accurately or alter a trade finance transaction dynamically as it progresses. For instance, in a digital data-rich world, it becomes possible to track an oil or consumer goods shipment around the world and change its value and insurance cost to the business as the ship nears its destination.

In a data-rich environment, Intraday liquidity management, optimized credit lines and inter-company funding will become possible for treasurers. The increased amount of tracking and other data made available, as paper gets eliminated, would mean that advanced analytics would have bigger pools to interrogate and more granular insights can be delivered.

In the future, open application programming interfaces (APIs) where Fintechs, other banks and non-traditional players can all access customer data – if they meet specific minimum security parameters – would mean the development of more diverse data-rich tools.

These developments are receiving support from emerging technologies and trends like artificial intelligence (AI) inspired data mining and Robotic Process Automation (RPA) tools. The increasing use of cloud computing and digital processes – not to mention the diminution of siloed systems – are all necessary first steps to feed these ‘big data’ tools.

Getting the most out of your IT overhaul

Before charging ahead with investment in advanced new technologies or open API schemes, however, corporate treasurers and their banking partners should first work out what they want to achieve by adopting new cloud-based systems and data-rich analytical tools. They need to align people, process and technology to get a clear Return on Investment (RoI).

Most companies prioritize automation of repetitive and non-core activities to achieve efficiency and use digitalization as a means to create a competitive advantage for sustainable sales growth. Such Digital Transformation projects are, however, plagued with familiar challenges that need addressing in the early stages. The most familiar obstacles are:

Legacy organizational models: Outdated working methodologies and outmoded siloed IT doesn’t promote shared objectives across sales and treasury, or encourage effective linkages with banks, payment processors and other financial supply chain partners. The models need overhauling, along with the IT infrastructure.

Align people, process and technology:It is important that this is done early in a digital transformation project as technology transformations are notorious for failing to deliver RoI. It happens because the end-stage goal and end-users were not identified correctly before implementation.

Train staff and users:Bad habits lead to process paralysis and low adoption of new technology. It’s important that staff and partners are trained to ensure they get the most out of new investments.

Following the above steps would ensure that corporate treasurers have an interconnected ecosystem that can scale up for the upcoming open API-enabled future and deliver real, graduated benefits.

Figure 2: An interconnected system starts with digitalization and the use of the cloud. It opens up the more effective use of analytics, AI, and so forth to deliver practical benefits. Source: Emirates NBD.

Conclusion

Companies in the UAE can expect to benefit from tech-savvy banks and financial supply chain partners in addition to government-supported Fintech hubs and digital initiatives such as the transition to a paperless economy, along with other advantages such as low tax and free trade zones that link with the wider world.

Accelerating business growth, improving operating efficiencies and supporting cross-border expansion plans, all while enhancing transparency and efficiency across the internal organization are real benefits that corporate treasuries can expect to access with Digital Transformation.

At Emirates NBD, our primary aim is to help firms improve their bottom line, and our approach of being a technology partner is designed to support treasurers all the way and help them gain credibility within their organizations to launch Digital Transformation projects that deliver enterprise-wide advantages.

Leave a Reply