Cash & Liquidity ManagementFXAn alternative calculation of the Black Scholes formula for effective hedging programmes

An alternative calculation of the Black Scholes formula for effective hedging programmes

Effective hedging programs to mitigate the impact of high inflation and a rampant US dollar require an understanding of option strategies and pricing formula, says former treasurer and treasury management consultant Walter Ochynski, while offering a fresh perspective on the Black Scholes model

The Black-Scholes model is one of the most important concepts in modern financial theory. Stochastic calculus is now taught in many MBA courses – this would not have happened if the Black Scholes model was not invented.

Although the Black Scholes model is so important and N(d1) and N(d2) are integral parts of this model, neither Black and Scholes nor Merton explained or interpreted the N(d1) or N(d2). Explanations in many textbooks are also very limited as far as the difference between N(d1) and N(d2) is concerned – Why are they different?

Cox and Rubinstein stated that the stock price x N(d1) is the present value of receiving the stock if and only if the option finishes in the money, and the discounted strike price x Nd2 is the present value of paying the strike price. I personally like the explanation provided by QuantPie.

It is quite unfortunate that they provided the explanation under the assumption that risk-free interest rate and foreign rate (or dividend rate) are zero. Many finance students are taught about stochastic PDE from which the Black Scholes formula is derived, Brownian motion, Wiener process etc. without proper explanation that the Black Scholes model elegantly reduces the stochastic impact, using dynamic delta hedging. Is the assumption of random walk really very important, if it can be hedged away?

The Black Scholes model is a convenient way to calculate the price of the option. In this article, I will show an alternative and simpler way to calculate option premium, which always leads to the same results as the Black Scholes model and shows the true difference between N(d1) and N(d2). I will also show that d1 and d2 are nothing else as Z-scores of two populations with different means.

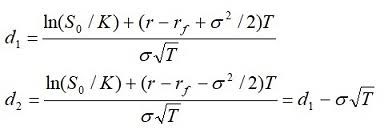

The normally used Black Scholes formula for dividend carrying assets or foreign exchange looks as follows:

The partial differential equation for which the above Black Scholes formula is the accepted solution has also a stochastic component. It is very often stated that Black Scholes PDE depends on random walk or Brownian motion. However, the random walk of the derivative instrument and the underlying asset is driven by the same random variable.

By applying delta hedging the two random walks – for option and underlying asset- offset each other. Delta hedging is a dynamic strategy, the delta hedge is only instantaneously risk-free, and it requires a continuous rebalancing of the portfolio. If transaction costs are significant then the frequent rebalancing necessary to maintain a delta neutral position renders the policy impractical.

Growth rate, which is a part of Black Scholes PDE, does not appear in the Black Scholes equation. The value of the option depends on the standard deviation of the asset price. Different investors, which may have very different estimates of the growth rate can still agree on the value of the option. The value of the option does not depend on the value of the underlying asset in the future.

The risk preferences are irrelevant because the risk can be hedged away with for example delta hedging. Whether the assets go up or down the value of the option remains the same. With the help of Excel, the potential future price development can be easily simulated and the costs of delta hedging remain the same, whether assets show positive or negative growth or no trend at all. The stochastic growth rate is replaced in the Black Scholes equation with deterministic interest rates, see formulas for d1 and d2. The option is calculated by applying the present value of the calculated return at expiry, no random walk anymore. The results can be ensured with an adequate delta hedging strategy, independently from asset price development in the future. The Black Scholes formula is agnostic as far as future asset price development is concerned. It depends however on the volatility of the underlying asset. Smart, effective hedging programs are only possible with the correct application of Black Scholes model.

If the Black Scholes model is asset price agnostic, what can N(d1) and N(d2) say about future price development?

I present now a model where N(d1) and N(d2) are two lognormal distributions with the same standard deviation but different means. N(d1) has a mean equal to the logarithm of the spot price plus half of the squared volatility plus risk-free rate minus dividend or foreign interest rate. In the N(d2) mean calculation the standard deviation is not added but subtracted. Please compare this with the formulas in the Black Scholes equation for d1 and d2. Quite often the d2 will not be calculated separately but you subtract from d1 volatility times square route of time. The two means differ by volatility^2 times time, I would guess if in the seventies of the last century Excel spreadsheet with the lognormal function would have been available, Black and Scholes would also apply the alternative calculation used in this model. In my view, it is easier to implement and comprehend. You can imagine N(d1) and N(d2) as two distributions with the same standard deviation but different means (see Graphic 1).

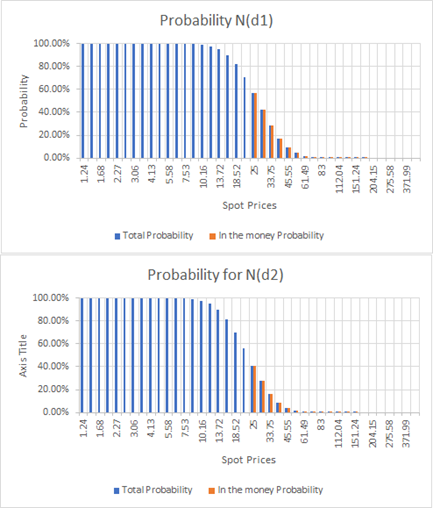

Graphic 1: Two distributions with the same standard deviations but different means

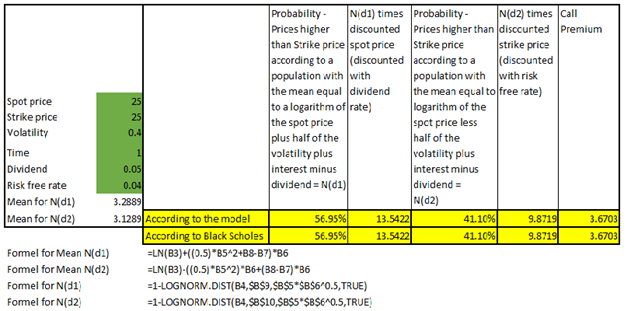

Table one shows the data used for the sample calculation. We see that the mean for N(d1) is bigger than for N(d2). For N(d1) half of the squared volatility has to be added and for the N(d2) subtracted. Mean characterizes the population. When the mean increases the population moves to the right, then when decreases the population moves to the left (see graphic 1). Both means are expressed as logarithms. Expressed as regular numbers they amount to e^3.2889 equals 26.8127 for the mean of N(d1) and 22.8482 for N(d2)[1]. Populations with the same standard deviations but different means cannot lead to the same results. Graphic 2 shows the lognormal cumulative distribution for 1-N(d1) and 1-N(d2). X-axes are not to scale. Using the spot price of 25 as the current price, there is almost no chance that prices will be lower than 1 according to the assumed volatility and other variables, see Graphic 2. I show here probabilities greater than… This means that there is almost a 100% chance that prices will be higher than 1.24, 1.68, etc. Prices of at least 18.52 can be expected according to N(d1) distribution with a probability of around 80% and according to N(d2) with a probability of around 70%. N(d1) and N(d2) are two different populations and depend on the provided data and not any future price development. We did not enter any data about potential asset price development in the future, Table 1.

Table 1: Input for Option calculation model

We have assumed 25 as the strike price. At the spot price of 25 option is at the money. What is the probability that prices according to the model can be expected to be higher than 25 at the maturity of the option? For 1-N(d1) it is a probability of 56.95% and for 1-N(d2) 41.10%. Both probabilities have nothing to do with the expected future prices but simply with the used assumptions. N(d1) and N(d2) have different assumptions about the mean and this creates different probabilities for the calculated spot prices when the option expires, see graphic 1 and check the probability of x=1 according to distribution with mean=0 and mean=3

When we want to calculate option prices using the probabilities according to the here presented alternative calculation we just need to enter a few simple formulas into the spreadsheet, the results are shown in table 2. They are exactly as per traditional Black Scholes model calculation.

This alternative calculation shows always the same results as the traditional Black Scholes calculation. It shows also that N(d1) and N(d2) cannot be any indication of future value of underlying assets but are just results based on two different lognormal distributions, which are an integral part of the Black Scholes model. Showing how these probabilities of the Lognormal distribution function differ, in dependence of standard deviation and mean, can better explain the meaning of N(d1) and N(d2). I assume everybody agrees that if populations have different standard deviations or means, they show different probabilities. This is self-evident from the here presented alternative option price calculation but not from traditional d1 and d2 in the Black Scholes equation and might be clear to statisticians but not to most treasurers. The model can also be used as an alternative way to calculate option prices, which can be easier implemented in excel or google sheets. Why Black and Scholes did not explain the meaning of N(d1) and N(d2)? I do not know.

Table 2: Alternative model to calculate the option premium

I can also show that d1 and d2 in the Black Scholes model are z scores of the populations presented here. We obtain z score when we subtract from the Logarithm of the strike price the mean and divide the results by the standard deviation. Z-score indicates where the particular data is situated measured in standard deviation and provides the corresponding probability.

I can show how we can transform Z-score into d1 in the Black Scholes formula. Ln of the Strike price less mean used in the model for d1 divided by the standard deviation.

To have the equation which can be used for periods below and above a year we had to multiply interest by the time involved (in years) and multiply the standard deviation by the square root of time. This is a logarithmic equation. We do not multiply interest but we add it or subtract it. We can subtract logarithms or divide the two values. I will use this rule for strike and spot price. But before I will multiply this equation by minus 1. (See above to find the probability of 1-z score, we used minus z-score)

I could perform a similar transformation for d2. The reader is encouraged to do it by himself.

Effective hedging is the priority of every treasurer and is not possible without full comprehension of the Black Scholes model.

Now everybody agrees with me that d1 and d2 are z scores of two different populations with the same standard deviation but different means. In the presented model I used the lognormal distribution function. I could also apply the normal distribution function as Black Scholes model does, but then for the x value in the function, I would have to use the logarithm of the strike price. The results remain the same. 50 years after the Black Scholes equation was invented we finally know the meaning of the N(d1) and N(d2) which are probabilities of two z-scores of two distributions with different means.

Graphic 2: Lognormal cumulative distribution for N(d2) and N(d1)

Is dynamic hedging according to delta defined as N(d1) the best hedging strategy in any circumstances? If future prices develop according to the distribution as per N(d2), then N(d2) might be a better hedging ratio. Understanding N(d1) and N(d2) as different distributions we could try to answer this question with a Monte Carlo simulation.

Leave a Reply