A treasurer’s perspective: The true cost of capital – MWACC investigated

Modified weighted average cost of capital (MWACC) is the internal hurdle rate a business should use to evaluate its own capital investments, explains Ben Walters, deputy treasurer at Compass Group

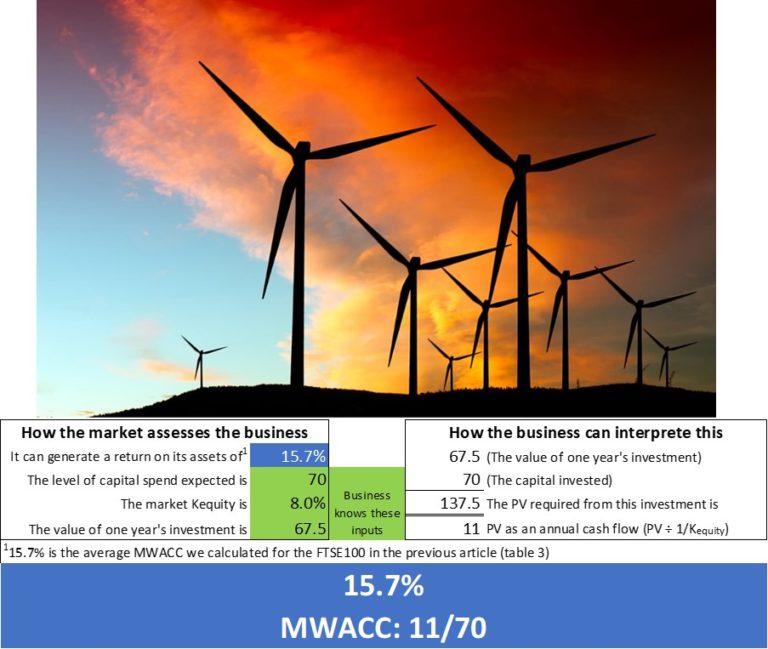

In the last article, I introduced a new concept for arriving at an internal target rate of return for the capital a business invests in its operations. This target – modified weighted average cost of capital(MWACC) – is derived from the market’s valuation of the business. This valuation invariably includes a substantial element of growth and by deciphering the message this gives can set a rate of return for its investments that matches these growth expectations. Figure one shows how the business can determine its MWACC from the market’s valuation of itself after applying some simple mathematics.

Figure one: the business must make 15% from its wind farm investments to justify its market price

If Figure 1 looks a little circular then that is exactly the point. The business is set the task of calculating the market’s assessment of the return it can make on its assets. When the business learns how to work this out it becomes its MWACC – the 15.7% that the market first thought of. From here the business can do the maths because it knows its valuation, its WACC, and the level of capital it is investing. These inputs are visible in the market or from its own business plan.

On the right-hand side of the table in figure one, the business must cover both the cost of its investments (70) and the value the market has assigned to it (67.5) as the additional value of the growth potential. This combined present value is 137.5, and when discounted at WACC results in an annual cash flow target of 11. MWACC is then derived by dividing 11 by the capital invested of 70, giving 15.7%. This is the implicit rate of return the market demands the business makes from its capital investments in order to justify the value of the business. Undershoot this target and the value of the business will fall, exceed it and the value of the business will rise.

MWACC FAQs

How should MWACC be used within the business?

MWACC is the correct discount rate to use in all NPV appraisals the business carries out. MWACC is not arbitrary, it has a tangible basis grounded in the market’s growth demands on the business. This gives the internal hurdle rate much more credibility than a rate plucked out of the air by head office.

What is the relationship between WACC and MWACC?

The more growth potential embedded in the market’s valuation of the business the higher its MWACC. A high element of growth potential as a proportion of total value will lead to a higher MWACC versus WACC.

The market’s message to the business is that it has a strong strategic position and can make a high rate of return from its assets. Where the gap between WACC and MWACC is much narrower the market is not assigning much value to the strategic position.

What do you need to measure MWACC?

MWACC is derived from easily available inputs. Financial information from the cash flow statement, market data such as share price and market capitalisation, an assessment of WACC, and either historic or expected levels of capital spend are all that is needed to calculate MWACC.

Does high MWACC penalise the more highly rated business compared to its competitors?

Do competitors “benefit” from a lower MWACC allowing them to pursue opportunities that the higher rated business must pass over? Well, the answer should be no, as long as the market has valued that business’s strategy and strengths correctly.

The challenge that a high MWACC poses for a business should be set against the strengths that the market perceives that business as possessing over its competitors. The market believes it can make better returns from the same economic environment than its competitors.

An analogy would be the superstar footballer with an astronomical value. Clearly, he is under pressure to deliver. However, if the valuation is correct, he should be able to do so by winning lots of trophies and repaying his club.

Using MWACC to identify value

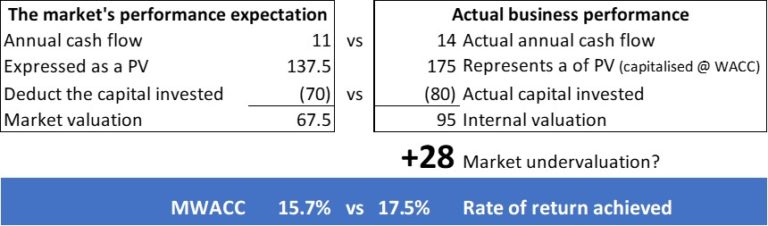

MWACC opens up several incredibly useful areas of analysis for the business. Figure two explains how it is an easy exercise to substitute actual performance into the calculation to derive the real rate of return achieved and compare this against the target MWACC. Some uses for this analysis include:

Value its own business units by comparing the returns made against the MWACC target. This guides capital allocation within the business and allows for a portfolio review of business units to determine where value is created or destroyed.

Set performance targets in its budgeting and planning process that meet or exceed its MWACC target and therefore create value. The rate of return on assets derived from MWACC can easily by expressed as an EBITDA, profit, or revenue target.

Within M&A activity in comparing a target business’ rate of return on its assets to the acquirer’s MWACC. Understanding how the target and acquirer’s rates of return from their assets differ can guide towards the correct valuation and potential synergy.

Overall business valuation: our example in figure two shows our business delivering a return of 17.5% based on its actual results which are higher than its MWACC of 15.7%. This in turn equates to a potential undervaluation of 28 by the market. Again useful for M&A, but as figure three demonstrates, this has much wider uses for investors in the stock market.

Figure two: reverse engineer our MWACC derivation technique to determine performance in value terms

Testing MWACC against actual performance

The MWACC concept can be thought of as simply breaking down the growth element of a business’ value into a rate of return on the capital invested that matches this valuation in present value terms.

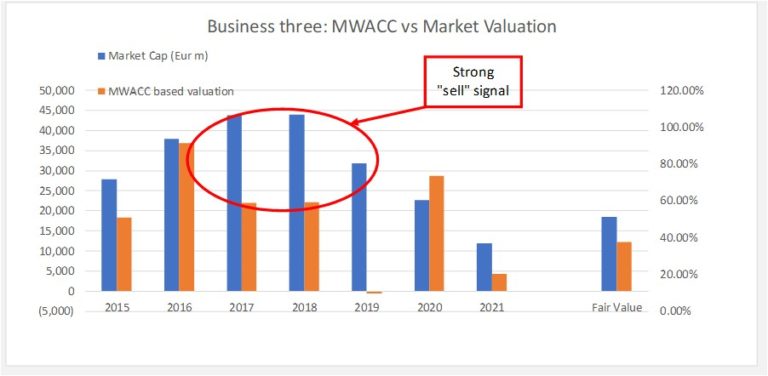

We can test the concept by looking at how the market valuation compares to a valuation derived from MWACC. Three listed businesses’ have been analysed to determine their MWACC-derived valuation and then compared to their market capitalisation. The results are shown in Figure 3 below.

Figure three: MWACC and market-derived valuations show alignment over time

All of the businesses analysed are large listed blue-chip concerns. Valuation correlations of between 46-85%, considered moderate to strong, provide substantial evidence that the market and MWACC-derived valuations move in synch over time.

Considering the huge number of external macro factors that affect the stock market and sectors within it, this level of correlation is effective proof that MWACC really measures value creation or destruction.

A little further analysis has been done looking into the buy and sell signals identified in figure three (see bottom box in table one). Buying into business one in 2015, or shorting business three in 2017 would have resulted in capital gains of 14-21% per annum even before any dividend payouts. Not a bad return at all.

Table one: Some results from comparing MWACC to market valuations

What figure three and table one prove is that MWACC really works. With confidence in the concept, the business can flow MWACC-based targets into its budgeting process. It can also use MWACC to assess its portfolio of business units, allocate capital to those that create value, and withdraw, fix or dispose of units that destroy value. MWACC can make an enormous contribution to the creation of value within the business.

This may not be traditional treasury, but it goes to the heart of the protection and enhancement of the value of capital which is a fundamental responsibility of the treasurer. Treasury is uniquely placed as both the liaison between the market and the business and the experts in valuation, to promote the use of MWACC within their business.

Figure three: MWACC and market-derived valuations show alignment over time

Figure three: MWACC and market-derived valuations show alignment over time

Leave a Reply